202

Garcilaso de la Vega

Commentarios Reales, 1722-1723.

Estimation: € 1,200 / $ 1,284

Garcilaso de la Vega

Primera parte de los commentarios reales, que tratan, de el origen de los incas, reies, que fueron del Perú. - Historia General del Peru. - Zus. 2 Werke in 1 Band. Madrid, N. R. Franco 1722-1723.

Zwei wertvolle Berichte aus erster Hand über das Inkareich.

Zweite Ausgaben, erschienen erstmals 1609 und 1617. Der "El Inca" genannte peruanische Schriftsteller und Historiker Garcilaso de la Vega (1539-1619) schrieb über die Geschichte der Inka aus der Erinnerung an die mündlichen Überlieferungen, die ihm aus seiner Familie und Ausbildung bekannt waren, ergänzt durch Auskünfte, die er bei in Peru lebenden Verwandten und Bekannten einholte. - "The Historia General has been defined the most genuinely American book that has ever been written, and perhaps the only one in which a reflection of the soul of the conquered races has survived" (Menendez y Pelayo). "Like the first part, the second is a commentary rather than a history; (the author) quotes largely from other writers always carefully indicating the quotations and naming the authors. But his memory was well stored with anecdotes that he had heard when a boy; and with these he enlivens the narrative" (J. Winsor, Narrative and Critical History of America II, p. 569).

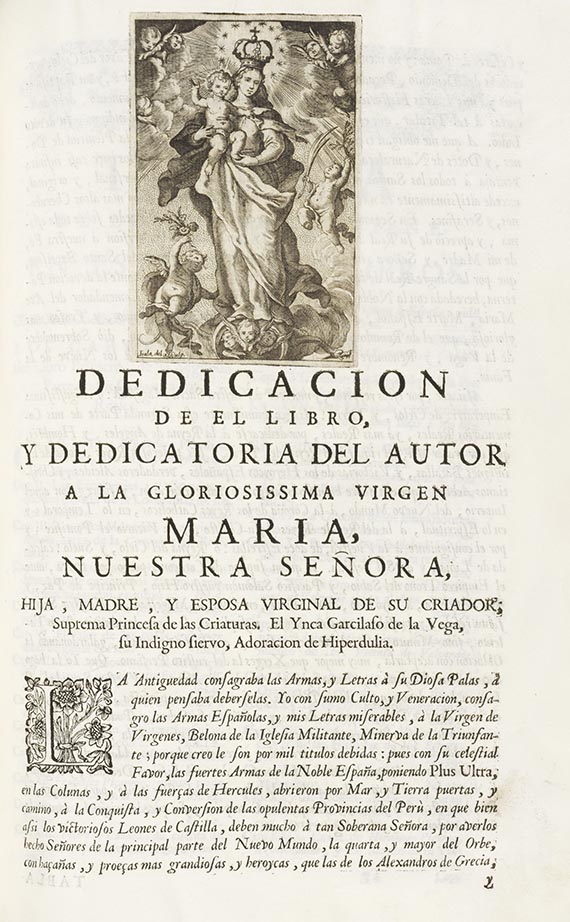

EINBAND: Gefleckter Lederband der Zeit mit reicher Rückenvergoldung und Rückenschild. 31 : 21 cm. - ILLUSTRATION: Mit 2 Holzschnitt-Vignetten auf den Titeln und 1 gest. Kopfvignette. - KOLLATION: 16 Bll., 351 S., 17 Bll. Register; 12 Bll., 505 S., 31 Bll. Register. - ZUSTAND: Letzte ca. 10 Bll. mit Braunfleck, Titel mit restaur. Einrissen, 1 Bl. mit mehreren Einrissen und kl. Eckabriß. Einbd. mit kl. Beschabungen. Insges. sauberes Exemplar. - PROVENIENZ: Gest. Wappenexlibris "Nil difficile volenti".

LITERATUR: Alden/Landis 723/58. - Palau 354791 und 354793. - Sabin 98757 und 98755.

Second edition of 2 indispensable first-hand accounts of the pre-conquest Inca Empire, the period of Spanish conquest and later civil war between Pizarro and Almagros, containing unique information and historical records available nowhere else. With together 2 woodcut title vignettes (woodcut on title of 2nd work shows Our Lady with the child and was repeated (but engraved) on top of 2nd leaf. Contemp. brown speckled calf with gilt spine and label on spine. - Last ca. 10 leaves with brown stain, title with restored tears, 1 leaf with several tears and small corner torn off. Binding with small scrapings. Overall a clean copy. Engr. armorial bookplate "Nil difficile volenti".(R)

Primera parte de los commentarios reales, que tratan, de el origen de los incas, reies, que fueron del Perú. - Historia General del Peru. - Zus. 2 Werke in 1 Band. Madrid, N. R. Franco 1722-1723.

Zwei wertvolle Berichte aus erster Hand über das Inkareich.

Zweite Ausgaben, erschienen erstmals 1609 und 1617. Der "El Inca" genannte peruanische Schriftsteller und Historiker Garcilaso de la Vega (1539-1619) schrieb über die Geschichte der Inka aus der Erinnerung an die mündlichen Überlieferungen, die ihm aus seiner Familie und Ausbildung bekannt waren, ergänzt durch Auskünfte, die er bei in Peru lebenden Verwandten und Bekannten einholte. - "The Historia General has been defined the most genuinely American book that has ever been written, and perhaps the only one in which a reflection of the soul of the conquered races has survived" (Menendez y Pelayo). "Like the first part, the second is a commentary rather than a history; (the author) quotes largely from other writers always carefully indicating the quotations and naming the authors. But his memory was well stored with anecdotes that he had heard when a boy; and with these he enlivens the narrative" (J. Winsor, Narrative and Critical History of America II, p. 569).

EINBAND: Gefleckter Lederband der Zeit mit reicher Rückenvergoldung und Rückenschild. 31 : 21 cm. - ILLUSTRATION: Mit 2 Holzschnitt-Vignetten auf den Titeln und 1 gest. Kopfvignette. - KOLLATION: 16 Bll., 351 S., 17 Bll. Register; 12 Bll., 505 S., 31 Bll. Register. - ZUSTAND: Letzte ca. 10 Bll. mit Braunfleck, Titel mit restaur. Einrissen, 1 Bl. mit mehreren Einrissen und kl. Eckabriß. Einbd. mit kl. Beschabungen. Insges. sauberes Exemplar. - PROVENIENZ: Gest. Wappenexlibris "Nil difficile volenti".

LITERATUR: Alden/Landis 723/58. - Palau 354791 und 354793. - Sabin 98757 und 98755.

Second edition of 2 indispensable first-hand accounts of the pre-conquest Inca Empire, the period of Spanish conquest and later civil war between Pizarro and Almagros, containing unique information and historical records available nowhere else. With together 2 woodcut title vignettes (woodcut on title of 2nd work shows Our Lady with the child and was repeated (but engraved) on top of 2nd leaf. Contemp. brown speckled calf with gilt spine and label on spine. - Last ca. 10 leaves with brown stain, title with restored tears, 1 leaf with several tears and small corner torn off. Binding with small scrapings. Overall a clean copy. Engr. armorial bookplate "Nil difficile volenti".(R)

202

Garcilaso de la Vega

Commentarios Reales, 1722-1723.

Estimation: € 1,200 / $ 1,284

Commission, taxes et droit de suite

Cet objet est offert avec imposition régulière.

Calcul en cas d'imposition régulière:

Prix d'adjudication jusqu'à 200 000 € : 25 % de commission majorée de la TVA légale

Prix d'adjudication supérieur à 200 000 € : montants partiels jusqu'à 200 000 € 25 % de commission, montants partiels supérieurs à 200 000 € : 20 % de commission, à chaque fois majorés de la TVA légale.

Calcul en cas de droit de suite:

Pour les œuvres originales d’arts plastiques et de photographie d’artistes vivants ou d’artistes décédés il y a moins de 70 ans, soumises au droit de suite, une rémunération au titre du droit de suite à hauteur des pourcentages indiqués au § 26, al. 2 de la loi allemande sur les droits d’auteur (UrhG) est facturée en sus pour compenser la rémunération liée au droit de suite due par le commissaire-priseur conformément au § 26 UrhG. À ce jour, elle est calculée comme suit :

4 pour cent pour la part du produit de la vente à partir de 400,00 euros et jusqu’à 50 000 euros,

3 pour cent supplémentaires pour la part du produit de la vente entre 50 000,01 et 200 000 euros,

1 pour cent supplémentaire pour la part entre 200 000,01 et 350 000 euros,

0,5 pour cent supplémentaire pour la part entre 350 000,01 et 500 000 euros et

0,25 pour cent supplémentaire pour la part au-delà de 500 000 euros.

Le total de la rémunération au titre du droit de suite pour une revente s’élève au maximum à 12 500 euros.

Calcul en cas d'imposition régulière:

Prix d'adjudication jusqu'à 200 000 € : 25 % de commission majorée de la TVA légale

Prix d'adjudication supérieur à 200 000 € : montants partiels jusqu'à 200 000 € 25 % de commission, montants partiels supérieurs à 200 000 € : 20 % de commission, à chaque fois majorés de la TVA légale.

Calcul en cas de droit de suite:

Pour les œuvres originales d’arts plastiques et de photographie d’artistes vivants ou d’artistes décédés il y a moins de 70 ans, soumises au droit de suite, une rémunération au titre du droit de suite à hauteur des pourcentages indiqués au § 26, al. 2 de la loi allemande sur les droits d’auteur (UrhG) est facturée en sus pour compenser la rémunération liée au droit de suite due par le commissaire-priseur conformément au § 26 UrhG. À ce jour, elle est calculée comme suit :

4 pour cent pour la part du produit de la vente à partir de 400,00 euros et jusqu’à 50 000 euros,

3 pour cent supplémentaires pour la part du produit de la vente entre 50 000,01 et 200 000 euros,

1 pour cent supplémentaire pour la part entre 200 000,01 et 350 000 euros,

0,5 pour cent supplémentaire pour la part entre 350 000,01 et 500 000 euros et

0,25 pour cent supplémentaire pour la part au-delà de 500 000 euros.

Le total de la rémunération au titre du droit de suite pour une revente s’élève au maximum à 12 500 euros.