Image du cadre

Raumbeispiel

427

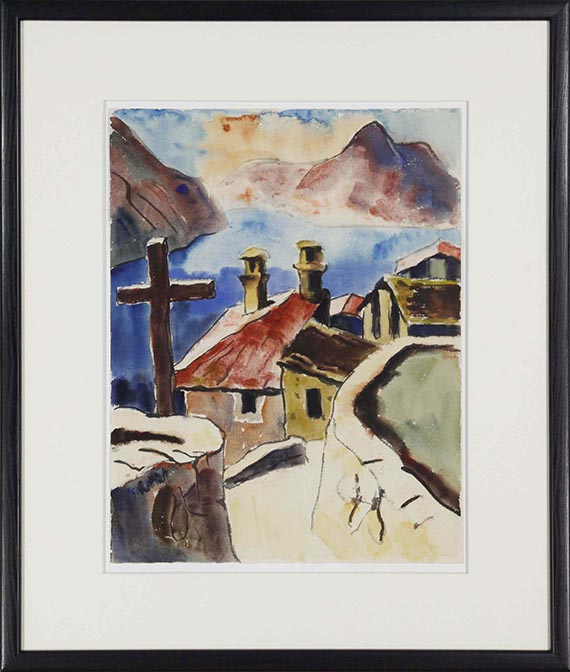

Karl Schmidt-Rottluff

Häuser im Tessin, 1928/29.

Watercolor and ink pen

Estimation: € 25,000 / $ 26,750

Häuser im Tessin. 1928/29.

Watercolor and ink pen.

Signed in lower left. On slightly structured wove paper. 59.5 x 46 cm (23.4 x 18.1 in), the full sheet. [CH].

• Between 1927 and 1929, Schmidt-Rottluff traveled to the Ticino several times and found inspiration for his vibrant watercolors in the mountainous landscape.

• The artist depicts the idyllic village and the view over Lake Lugano from an elevated vantage point.

• He dissolves the scenery into reduced forms and high-contrast, at times bold and then again delicately washed fields of color.

The work is documented in the archive of the Karl and Emy Schmidt-Rottluff Foundation, Berlin.

PROVENANCE: Hermann Gerlinger Collection, Würzburg (with the collector's stamp, Lugt 6032).

EXHIBITION: Schleswig-Holsteinisches Landesmuseum, Schloss Gottorf, Schleswig (permanent loan from the Hermann Gerlinger Collection, 1995-2001).

Kunstmuseum Moritzburg, Halle an der Saale (permanent loan from the Hermann Gerlinger Collection, 2001-2017).

Buchheim Museum, Bernried (permanent loan from the Hermann Gerlinger Collection, 2017-2022).

LITERATURE: Heinz Spielmann (ed.), Die Maler der Brücke. Sammlung Hermann Gerlinger, Stuttgart 1995, p. 411, SHG no. 735 (illu. in color).

Hermann Gerlinger, Katja Schneider (eds.), Die Maler der Brücke. Inventory catalog Hermann Gerlinger Collection, Halle (Saale) 2005, pp. 112f., SHG no. 251 (illu. in color).

Called up: June 8, 2024 - ca. 17.36 h +/- 20 min.

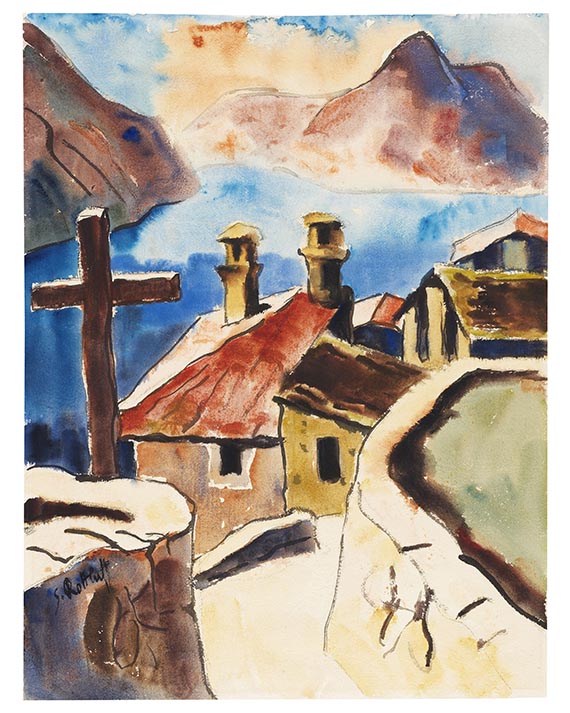

Watercolor and ink pen.

Signed in lower left. On slightly structured wove paper. 59.5 x 46 cm (23.4 x 18.1 in), the full sheet. [CH].

• Between 1927 and 1929, Schmidt-Rottluff traveled to the Ticino several times and found inspiration for his vibrant watercolors in the mountainous landscape.

• The artist depicts the idyllic village and the view over Lake Lugano from an elevated vantage point.

• He dissolves the scenery into reduced forms and high-contrast, at times bold and then again delicately washed fields of color.

The work is documented in the archive of the Karl and Emy Schmidt-Rottluff Foundation, Berlin.

PROVENANCE: Hermann Gerlinger Collection, Würzburg (with the collector's stamp, Lugt 6032).

EXHIBITION: Schleswig-Holsteinisches Landesmuseum, Schloss Gottorf, Schleswig (permanent loan from the Hermann Gerlinger Collection, 1995-2001).

Kunstmuseum Moritzburg, Halle an der Saale (permanent loan from the Hermann Gerlinger Collection, 2001-2017).

Buchheim Museum, Bernried (permanent loan from the Hermann Gerlinger Collection, 2017-2022).

LITERATURE: Heinz Spielmann (ed.), Die Maler der Brücke. Sammlung Hermann Gerlinger, Stuttgart 1995, p. 411, SHG no. 735 (illu. in color).

Hermann Gerlinger, Katja Schneider (eds.), Die Maler der Brücke. Inventory catalog Hermann Gerlinger Collection, Halle (Saale) 2005, pp. 112f., SHG no. 251 (illu. in color).

Called up: June 8, 2024 - ca. 17.36 h +/- 20 min.

In the 1920s, Schmidt-Rottluff entered a phase of extensive travel:

"In 1923, he set off towards southern Europe for the first time to explore Italy in the company of his sculptor friends Georg Kolbe and Richard Scheibe. This was followed by trips to Paris (1924), Dalmatia (1925), and the Swiss Ticino (1927-1929). The inspiration the artist found there is reflected in the increased production of landscape paintings starting midway through the decade. Around this time, a further stylistic transformation became apparent: The works are characterized by a greater closeness to nature, the forms become more plastic and voluminous, and the color loses its luminosity and gets more nuanced, giving the works a more harmonious and calmer effect. Schmidt-Rottluff's turn towards a more natural, sculptural style is linked to his first trip to Italy and was encouraged by his sculptor friends. Karl Brix wrote about the "transformation of Schmidt-Rottluff's art": "He had a strong inner relationship to nature, deeply experiencing its wealth of forms as reality, as a spatial and organic unity." (quoted from Magdalene Schlösser, Landschaft, in: Magdalena Möller (ed.), Karl Schmidt-Rottluff. Landscape, Figure, Still Life, 2014, p. 27)

"In 1923, he set off towards southern Europe for the first time to explore Italy in the company of his sculptor friends Georg Kolbe and Richard Scheibe. This was followed by trips to Paris (1924), Dalmatia (1925), and the Swiss Ticino (1927-1929). The inspiration the artist found there is reflected in the increased production of landscape paintings starting midway through the decade. Around this time, a further stylistic transformation became apparent: The works are characterized by a greater closeness to nature, the forms become more plastic and voluminous, and the color loses its luminosity and gets more nuanced, giving the works a more harmonious and calmer effect. Schmidt-Rottluff's turn towards a more natural, sculptural style is linked to his first trip to Italy and was encouraged by his sculptor friends. Karl Brix wrote about the "transformation of Schmidt-Rottluff's art": "He had a strong inner relationship to nature, deeply experiencing its wealth of forms as reality, as a spatial and organic unity." (quoted from Magdalene Schlösser, Landschaft, in: Magdalena Möller (ed.), Karl Schmidt-Rottluff. Landscape, Figure, Still Life, 2014, p. 27)

427

Karl Schmidt-Rottluff

Häuser im Tessin, 1928/29.

Watercolor and ink pen

Estimation: € 25,000 / $ 26,750

Commission, taxes et droit de suite

Cet objet est offert avec imposition régulière ou avec imposition différentielle.

Calcul en cas d'imposition différentielle:

Prix d’adjudication jusqu’à 800 000 euros : frais de vente 32 %.

Des frais de vente de 27% sont facturés sur la partie du prix d’adjudication dépassant 800 000 euros. Ils sont additionnés aux frais de vente dus pour la partie du prix d’adjudication allant jusqu’à 800 000 euros.

Des frais de vente de 22% sont facturés sur la partie du prix d’adjudication dépassant 4 000 000 euros. Ils sont additionnés aux frais de vente dus pour la partie du prix d’adjudication allant jusqu’à 4 000 000 euros.

Le prix de vente inclut la taxe sur la valeur ajoutée, actuellement de 19%.

Calcul en cas d'imposition régulière:

Prix d'adjudication jusqu'à 800 000 € : 27 % de commission majorée de la TVA légale

Prix d'adjudication supérieur à 800 000 € : montants partiels jusqu'à 800 000 € 27 % de commission, montants partiels supérieurs à 800 000 € : 21 % de commission, à chaque fois majorés de la TVA légale.

Prix d'adjudication supérieur à 4.000 000 € : montants partiels supérieurs à 4.000 000 € : 15 % de commission, à chaque fois majorés de la TVA légale.

Si vous souhaitez appliquer l'imposition régulière, merci de bien vouloir le communiquer par écrit avant la facturation.

Calcul en cas de droit de suite:

Pour les œuvres originales d’arts plastiques et de photographie d’artistes vivants ou d’artistes décédés il y a moins de 70 ans, soumises au droit de suite, une rémunération au titre du droit de suite à hauteur des pourcentages indiqués au § 26, al. 2 de la loi allemande sur les droits d’auteur (UrhG) est facturée en sus pour compenser la rémunération liée au droit de suite due par le commissaire-priseur conformément au § 26 UrhG. À ce jour, elle est calculée comme suit :

4 pour cent pour la part du produit de la vente à partir de 400,00 euros et jusqu’à 50 000 euros,

3 pour cent supplémentaires pour la part du produit de la vente entre 50 000,01 et 200 000 euros,

1 pour cent supplémentaire pour la part entre 200 000,01 et 350 000 euros,

0,5 pour cent supplémentaire pour la part entre 350 000,01 et 500 000 euros et

0,25 pour cent supplémentaire pour la part au-delà de 500 000 euros.

Le total de la rémunération au titre du droit de suite pour une revente s’élève au maximum à 12 500 euros.

Calcul en cas d'imposition différentielle:

Prix d’adjudication jusqu’à 800 000 euros : frais de vente 32 %.

Des frais de vente de 27% sont facturés sur la partie du prix d’adjudication dépassant 800 000 euros. Ils sont additionnés aux frais de vente dus pour la partie du prix d’adjudication allant jusqu’à 800 000 euros.

Des frais de vente de 22% sont facturés sur la partie du prix d’adjudication dépassant 4 000 000 euros. Ils sont additionnés aux frais de vente dus pour la partie du prix d’adjudication allant jusqu’à 4 000 000 euros.

Le prix de vente inclut la taxe sur la valeur ajoutée, actuellement de 19%.

Calcul en cas d'imposition régulière:

Prix d'adjudication jusqu'à 800 000 € : 27 % de commission majorée de la TVA légale

Prix d'adjudication supérieur à 800 000 € : montants partiels jusqu'à 800 000 € 27 % de commission, montants partiels supérieurs à 800 000 € : 21 % de commission, à chaque fois majorés de la TVA légale.

Prix d'adjudication supérieur à 4.000 000 € : montants partiels supérieurs à 4.000 000 € : 15 % de commission, à chaque fois majorés de la TVA légale.

Si vous souhaitez appliquer l'imposition régulière, merci de bien vouloir le communiquer par écrit avant la facturation.

Calcul en cas de droit de suite:

Pour les œuvres originales d’arts plastiques et de photographie d’artistes vivants ou d’artistes décédés il y a moins de 70 ans, soumises au droit de suite, une rémunération au titre du droit de suite à hauteur des pourcentages indiqués au § 26, al. 2 de la loi allemande sur les droits d’auteur (UrhG) est facturée en sus pour compenser la rémunération liée au droit de suite due par le commissaire-priseur conformément au § 26 UrhG. À ce jour, elle est calculée comme suit :

4 pour cent pour la part du produit de la vente à partir de 400,00 euros et jusqu’à 50 000 euros,

3 pour cent supplémentaires pour la part du produit de la vente entre 50 000,01 et 200 000 euros,

1 pour cent supplémentaire pour la part entre 200 000,01 et 350 000 euros,

0,5 pour cent supplémentaire pour la part entre 350 000,01 et 500 000 euros et

0,25 pour cent supplémentaire pour la part au-delà de 500 000 euros.

Le total de la rémunération au titre du droit de suite pour une revente s’élève au maximum à 12 500 euros.