Raumbeispiel

416

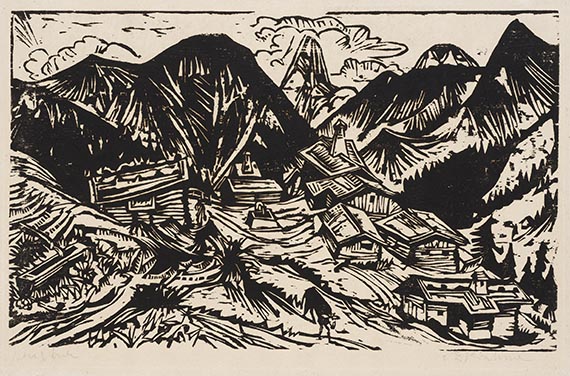

Ernst Ludwig Kirchner

Stafelalp mit Tinzenhorn, 1917.

Woodcut

Estimation: € 25,000 / $ 26,750

Stafelalp mit Tinzenhorn. 1917.

Woodcut.

Signed and inscribed "Handdruck". From an edition of only 21 known copies. On laminated blotting paper. 34.5 x 55.5 cm (13.5 x 21.8 in). Sheet: 39,3 x 58,4 cm (15,4 x 22,9 in).

The work is registered in Hermann Gerlinger Collection under the number SHG 775a. [CH].

• Hand-printed by the artist.

• During Kirchner's very first stay on the Stafelalp (above Davos) in 1917, he created 13 woodcuts, which are among the highlights of his oeuvre.

• Woodcuts play a particularly important role in Ernst Ludwig Kirchner's rich graphic oeuvre.

• Extremely detailed and very elaborate compositions.

• Only three copies of this woodcut have been offered on the international auction market in the last 20 years (source: artprice.com).

• Many of the 21 known copies of this woodcut are museum-owned, including the Museum of Fine Arts in Boston, the Philadelphia Museum of Art, the New York Public Library, the Albertina in Vienna, the Staatliche Museen zu Berlin, the Kunstmuseum Bern, the Stiftung Museum Kunstpalast, Düsseldorf, and the Kunstmuseum Winterthur.

PROVENANCE: Presumably Dr. Christian Adolf Isermeyer Collection, Berlin/Hamburg (with a hand-written ownershipnote on the reverse).

Hermann Gerlinger Collection, Würzburg (acquired in 2002, Galerie Kornfeld, Bern, with the collector's stamp, Lugt 6032).

EXHIBITION: Buchheim Museum, Bernried (permanent loan from the Hermann Gerlinger Collection, 2017-2022.

LITERATURE: Günther Gercken, Ernst Ludwig Kirchner. Kritisches Werkverzeichnis der Druckgraphik, vol. 4 (1917-1919), Bern 2015, no. 854 I (of II, illu.).

Annemarie and Wolf-Dieter Dube, E. L. Kirchner. Das graphische Werk, Munich 1967, no. H 301.

Gustav Schiefler, Die Graphik Ernst Ludwig Kirchners, vol. 2 (1917-1927), Berlin-Charlottenburg 1931, no. H 279.

- -

Galerie Kornfeld, Bern, 229th auction (Ist part), 175 ausgewählte Werke des 19. und 20. Jahrhunderts, June 21, 2002, lot 89 (full-page illu.).

Called up: June 8, 2024 - ca. 17.21 h +/- 20 min.

Woodcut.

Signed and inscribed "Handdruck". From an edition of only 21 known copies. On laminated blotting paper. 34.5 x 55.5 cm (13.5 x 21.8 in). Sheet: 39,3 x 58,4 cm (15,4 x 22,9 in).

The work is registered in Hermann Gerlinger Collection under the number SHG 775a. [CH].

• Hand-printed by the artist.

• During Kirchner's very first stay on the Stafelalp (above Davos) in 1917, he created 13 woodcuts, which are among the highlights of his oeuvre.

• Woodcuts play a particularly important role in Ernst Ludwig Kirchner's rich graphic oeuvre.

• Extremely detailed and very elaborate compositions.

• Only three copies of this woodcut have been offered on the international auction market in the last 20 years (source: artprice.com).

• Many of the 21 known copies of this woodcut are museum-owned, including the Museum of Fine Arts in Boston, the Philadelphia Museum of Art, the New York Public Library, the Albertina in Vienna, the Staatliche Museen zu Berlin, the Kunstmuseum Bern, the Stiftung Museum Kunstpalast, Düsseldorf, and the Kunstmuseum Winterthur.

PROVENANCE: Presumably Dr. Christian Adolf Isermeyer Collection, Berlin/Hamburg (with a hand-written ownershipnote on the reverse).

Hermann Gerlinger Collection, Würzburg (acquired in 2002, Galerie Kornfeld, Bern, with the collector's stamp, Lugt 6032).

EXHIBITION: Buchheim Museum, Bernried (permanent loan from the Hermann Gerlinger Collection, 2017-2022.

LITERATURE: Günther Gercken, Ernst Ludwig Kirchner. Kritisches Werkverzeichnis der Druckgraphik, vol. 4 (1917-1919), Bern 2015, no. 854 I (of II, illu.).

Annemarie and Wolf-Dieter Dube, E. L. Kirchner. Das graphische Werk, Munich 1967, no. H 301.

Gustav Schiefler, Die Graphik Ernst Ludwig Kirchners, vol. 2 (1917-1927), Berlin-Charlottenburg 1931, no. H 279.

- -

Galerie Kornfeld, Bern, 229th auction (Ist part), 175 ausgewählte Werke des 19. und 20. Jahrhunderts, June 21, 2002, lot 89 (full-page illu.).

Called up: June 8, 2024 - ca. 17.21 h +/- 20 min.

Kirchner arrived in Davos for the second time on May 8, 1917 to, as he wrote to his friend, the architect and designer Henry van de Velde, "complete my cure". During the summer, Kirchner lived with a nurse in the "Rüesch Hut" on the Stafelalp above Frauenkirch. Although he suffered from paralysis and was unable to write his own letters, he created landscapes and portraits of his new living environment that were characterized by an unbroken, elemental spirit of survival. And yet, Kirchner still had nightmarish fears and could not find peace. After a visit to the Stafelalp, Henry van de Velde persuaded Kirchner to confide in the psychiatrist and psychoanalyst Ludwig Binswanger. From mid-September 1917, Kirchner spent ten months at the Bellevue Sanatorium in Kreuzlingen on Lake Constance. Impressed by the nature that he saw right before his eyes, Kirchner depicted the steep alpine meadows with the "Alphütten", his view gliding across the gently rolling meadows interspersed with coarse rocks and weather-beaten wooden huts, sketching the narrow paths along the slope up to the nearby mountain plateau with more huts, giving contour to the forests and pastures. And Kirchner marked the mountain backdrop "Altein" on the other side of the valley with the omnipresent, striking Tinzenhorn, a mountain that towers over Kirchner's landscapes like a landmark. One can sense Kirchner's struggle to convey his fascination for the new mountain world in the woodcut, to 'reinvent' nature in detail. For Kirchner, the mountain dwellers he photographed became friends, whose habitat he commemorated in his early Davos landscapes. Kirchner also photographed the Stafelalp in the view from his summer hut and adopted the motifs for his view of the mountain village, as is the case with this large woodcut from 1917. Kirchner increasingly developed his Davos style and distanced himself from the original "metropolitan expressionism" of the Dresden and Berlin. [MvL]

416

Ernst Ludwig Kirchner

Stafelalp mit Tinzenhorn, 1917.

Woodcut

Estimation: € 25,000 / $ 26,750

Commission, taxes et droit de suite

Cet objet est offert avec imposition régulière ou avec imposition différentielle.

Calcul en cas d'imposition différentielle:

Prix d’adjudication jusqu’à 800 000 euros : frais de vente 32 %.

Des frais de vente de 27% sont facturés sur la partie du prix d’adjudication dépassant 800 000 euros. Ils sont additionnés aux frais de vente dus pour la partie du prix d’adjudication allant jusqu’à 800 000 euros.

Des frais de vente de 22% sont facturés sur la partie du prix d’adjudication dépassant 4 000 000 euros. Ils sont additionnés aux frais de vente dus pour la partie du prix d’adjudication allant jusqu’à 4 000 000 euros.

Le prix de vente inclut la taxe sur la valeur ajoutée, actuellement de 19%.

Calcul en cas d'imposition régulière:

Prix d'adjudication jusqu'à 800 000 € : 27 % de commission majorée de la TVA légale

Prix d'adjudication supérieur à 800 000 € : montants partiels jusqu'à 800 000 € 27 % de commission, montants partiels supérieurs à 800 000 € : 21 % de commission, à chaque fois majorés de la TVA légale.

Prix d'adjudication supérieur à 4.000 000 € : montants partiels supérieurs à 4.000 000 € : 15 % de commission, à chaque fois majorés de la TVA légale.

Si vous souhaitez appliquer l'imposition régulière, merci de bien vouloir le communiquer par écrit avant la facturation.

Calcul en cas de droit de suite:

Pour les œuvres originales d’arts plastiques et de photographie d’artistes vivants ou d’artistes décédés il y a moins de 70 ans, soumises au droit de suite, une rémunération au titre du droit de suite à hauteur des pourcentages indiqués au § 26, al. 2 de la loi allemande sur les droits d’auteur (UrhG) est facturée en sus pour compenser la rémunération liée au droit de suite due par le commissaire-priseur conformément au § 26 UrhG. À ce jour, elle est calculée comme suit :

4 pour cent pour la part du produit de la vente à partir de 400,00 euros et jusqu’à 50 000 euros,

3 pour cent supplémentaires pour la part du produit de la vente entre 50 000,01 et 200 000 euros,

1 pour cent supplémentaire pour la part entre 200 000,01 et 350 000 euros,

0,5 pour cent supplémentaire pour la part entre 350 000,01 et 500 000 euros et

0,25 pour cent supplémentaire pour la part au-delà de 500 000 euros.

Le total de la rémunération au titre du droit de suite pour une revente s’élève au maximum à 12 500 euros.

Calcul en cas d'imposition différentielle:

Prix d’adjudication jusqu’à 800 000 euros : frais de vente 32 %.

Des frais de vente de 27% sont facturés sur la partie du prix d’adjudication dépassant 800 000 euros. Ils sont additionnés aux frais de vente dus pour la partie du prix d’adjudication allant jusqu’à 800 000 euros.

Des frais de vente de 22% sont facturés sur la partie du prix d’adjudication dépassant 4 000 000 euros. Ils sont additionnés aux frais de vente dus pour la partie du prix d’adjudication allant jusqu’à 4 000 000 euros.

Le prix de vente inclut la taxe sur la valeur ajoutée, actuellement de 19%.

Calcul en cas d'imposition régulière:

Prix d'adjudication jusqu'à 800 000 € : 27 % de commission majorée de la TVA légale

Prix d'adjudication supérieur à 800 000 € : montants partiels jusqu'à 800 000 € 27 % de commission, montants partiels supérieurs à 800 000 € : 21 % de commission, à chaque fois majorés de la TVA légale.

Prix d'adjudication supérieur à 4.000 000 € : montants partiels supérieurs à 4.000 000 € : 15 % de commission, à chaque fois majorés de la TVA légale.

Si vous souhaitez appliquer l'imposition régulière, merci de bien vouloir le communiquer par écrit avant la facturation.

Calcul en cas de droit de suite:

Pour les œuvres originales d’arts plastiques et de photographie d’artistes vivants ou d’artistes décédés il y a moins de 70 ans, soumises au droit de suite, une rémunération au titre du droit de suite à hauteur des pourcentages indiqués au § 26, al. 2 de la loi allemande sur les droits d’auteur (UrhG) est facturée en sus pour compenser la rémunération liée au droit de suite due par le commissaire-priseur conformément au § 26 UrhG. À ce jour, elle est calculée comme suit :

4 pour cent pour la part du produit de la vente à partir de 400,00 euros et jusqu’à 50 000 euros,

3 pour cent supplémentaires pour la part du produit de la vente entre 50 000,01 et 200 000 euros,

1 pour cent supplémentaire pour la part entre 200 000,01 et 350 000 euros,

0,5 pour cent supplémentaire pour la part entre 350 000,01 et 500 000 euros et

0,25 pour cent supplémentaire pour la part au-delà de 500 000 euros.

Le total de la rémunération au titre du droit de suite pour une revente s’élève au maximum à 12 500 euros.