Autre image

Raumbeispiel

412

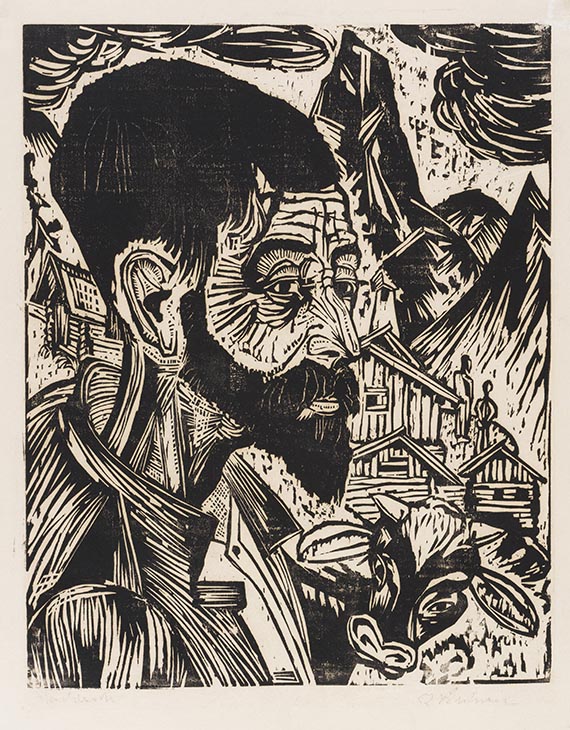

Ernst Ludwig Kirchner

Sennkopf (Martin Schmid), 1917.

Woodcut

Estimation: € 20,000 / $ 21,400

Sennkopf (Martin Schmid). 1917.

Woodcut.

Signed and inscribed "Handdruck". One of 17 known copies from the first printing stater. On blotting paper. 50 x 39.5 cm (19.6 x 15.5 in). Sheet: 57,5 x 44 cm (22,6 x 17,3 in).

[CH].

• Impressive format.

• During Kirchner's very first stay on the Stafelalp in 1917, he created 13 woodcuts, which rank among the highlights of Kirchner's oeuvre.

• One of the best-known print portraits from the Davos period.

• Based on a photograph Kirchner took of the Davos farmer Martin Schmid (Roland Scotti, E. L. Kirchner. Das fotografische Werk, Davos 2005, cat. no. 66).

• As the artist did not yet have a printing press at his disposal in Davos, he made the print from the wooden blocks by hand using a roller and bone folder, so that each copy varies slightly in the application of the ink and in its character.

• Eight copies of this woodcut are museum-owned: Rijksmuseum Amsterdam, Art Institute of Chicago, Harvard Art Museum, Cambridge/Mass., Kirchner Museum, Davos, Kunstmuseum Bern, Kupferstichkabinett of the Staatl. Museen zu Berlin, Stiftung Museum Kunstpalast, Düsseldorf, and the Germanisches Nationalmuseum, Nuremberg.

PROVENANCE: Hermann Gerlinger Collection, Würzburg (with the collector's stamp, Lugt 6032).

EXHIBITION: Schleswig-Holsteinisches Landesmuseum, Schloss Gottorf, Schleswig (permanent loan from the Hermann Gerlinger Collection, 1995-2001).

Kunstmuseum Moritzburg, Halle an der Saale (permanent loan from the Hermann Gerlinger Collection, 2001-2017).

Buchheim Museum, Bernried (permanent loan from the Hermann Gerlinger Collection, 2017-2022).

Expressiv! Die Künstler der Brücke. Die Sammlung Hermann Gerlinger, Albertina Vienna, June 1 - August 26, 2007, p. 272, cat. no. 174 (full-page illu., p. 273).

LITERATURE: Gustav Schiefler, Die Graphik Ernst Ludwig Kirchners, vol. 2 (1917-1927), Berlin-Charlottenburg 1931, no. H 277.

Annemarie and Wolf-Dieter Dube, E. L. Kirchner. Das graphische Werk, Munich 1967, no. H 308 I (of II).

Günther Gercken, Ernst Ludwig Kirchner. Kritisches Werkverzeichnis der Druckgraphik, vol. 4 (1917-1919), Bern 2015, no. 859 I (of II, illu.).

- -

Kunsthaus Lempertz, Cologne, 698th auction, Moderne Kunst, December 4, 1993, lot 250 (illu., plate 104).

Heinz Spielmann (ed.), Die Maler der Brücke. Sammlung Hermann Gerlinger, Stuttgart 1995, p. 267, SHG no. 389 (illu., p. 266).

Hermann Gerlinger, Katja Schneider (eds.), Die Maler der Brücke. Inventory catalog Hermann Gerlinger Collection, Halle (Saale) 2005, p. 345, SHG no. 776 (illu.).

Called up: June 8, 2024 - ca. 17.16 h +/- 20 min.

Woodcut.

Signed and inscribed "Handdruck". One of 17 known copies from the first printing stater. On blotting paper. 50 x 39.5 cm (19.6 x 15.5 in). Sheet: 57,5 x 44 cm (22,6 x 17,3 in).

[CH].

• Impressive format.

• During Kirchner's very first stay on the Stafelalp in 1917, he created 13 woodcuts, which rank among the highlights of Kirchner's oeuvre.

• One of the best-known print portraits from the Davos period.

• Based on a photograph Kirchner took of the Davos farmer Martin Schmid (Roland Scotti, E. L. Kirchner. Das fotografische Werk, Davos 2005, cat. no. 66).

• As the artist did not yet have a printing press at his disposal in Davos, he made the print from the wooden blocks by hand using a roller and bone folder, so that each copy varies slightly in the application of the ink and in its character.

• Eight copies of this woodcut are museum-owned: Rijksmuseum Amsterdam, Art Institute of Chicago, Harvard Art Museum, Cambridge/Mass., Kirchner Museum, Davos, Kunstmuseum Bern, Kupferstichkabinett of the Staatl. Museen zu Berlin, Stiftung Museum Kunstpalast, Düsseldorf, and the Germanisches Nationalmuseum, Nuremberg.

PROVENANCE: Hermann Gerlinger Collection, Würzburg (with the collector's stamp, Lugt 6032).

EXHIBITION: Schleswig-Holsteinisches Landesmuseum, Schloss Gottorf, Schleswig (permanent loan from the Hermann Gerlinger Collection, 1995-2001).

Kunstmuseum Moritzburg, Halle an der Saale (permanent loan from the Hermann Gerlinger Collection, 2001-2017).

Buchheim Museum, Bernried (permanent loan from the Hermann Gerlinger Collection, 2017-2022).

Expressiv! Die Künstler der Brücke. Die Sammlung Hermann Gerlinger, Albertina Vienna, June 1 - August 26, 2007, p. 272, cat. no. 174 (full-page illu., p. 273).

LITERATURE: Gustav Schiefler, Die Graphik Ernst Ludwig Kirchners, vol. 2 (1917-1927), Berlin-Charlottenburg 1931, no. H 277.

Annemarie and Wolf-Dieter Dube, E. L. Kirchner. Das graphische Werk, Munich 1967, no. H 308 I (of II).

Günther Gercken, Ernst Ludwig Kirchner. Kritisches Werkverzeichnis der Druckgraphik, vol. 4 (1917-1919), Bern 2015, no. 859 I (of II, illu.).

- -

Kunsthaus Lempertz, Cologne, 698th auction, Moderne Kunst, December 4, 1993, lot 250 (illu., plate 104).

Heinz Spielmann (ed.), Die Maler der Brücke. Sammlung Hermann Gerlinger, Stuttgart 1995, p. 267, SHG no. 389 (illu., p. 266).

Hermann Gerlinger, Katja Schneider (eds.), Die Maler der Brücke. Inventory catalog Hermann Gerlinger Collection, Halle (Saale) 2005, p. 345, SHG no. 776 (illu.).

Called up: June 8, 2024 - ca. 17.16 h +/- 20 min.

During his first stay on the Stafelalp in 1917, Kirchner made a woodcut of the alpine farmer Martin Schmid, a striking document of Kirchner's portrait art with the fascinating Tinzenhorn in the background. And Kirchner not only photographed him, but also his wife, Anna, with their two sons Martin and Hermann, presumably in the summer of 1917. Traces of snow between the beams allow the photo to be dated to the winter of 1918/19. Kirchner returned to Davos in July 1918 after his stay at the sanatorium in Kreuzlingen and lived in the hut that Martin Schmid let him use on the Stafelalp. In September 1920, Kirchner moved into the winter-proof farmhouse "In den Lärchen", which belonged to the Müller family. Hence, each residence is associated with a large number of works, and the variety of media used is also astonishing: in addition to oil paintings, he created woodcuts, etchings, watercolors, drawings, wooden sculptures and carpets. Despite his mental distress and partial paralysis, the first Davos period was extremely fruitful. Kirchner refined his Davos style and increasingly distanced himself from the original "Brücke" style of the Dresden and Berlin periods. [MvL]

412

Ernst Ludwig Kirchner

Sennkopf (Martin Schmid), 1917.

Woodcut

Estimation: € 20,000 / $ 21,400

Commission, taxes et droit de suite

Cet objet est offert avec imposition régulière ou avec imposition différentielle.

Calcul en cas d'imposition différentielle:

- Prix d’adjudication jusqu’à 800 000 euros : frais de vente 32 %.

- Des frais de vente de 27% sont facturés sur la partie du prix d’adjudication dépassant 800 000 euros. Ils sont additionnés aux frais de vente dus pour la partie du prix d’adjudication allant jusqu’à 800 000 euros.

- Des frais de vente de 22% sont facturés sur la partie du prix d’adjudication dépassant 4 000 000 euros. Ils sont additionnés aux frais de vente dus pour la partie du prix d’adjudication allant jusqu’à 4 000 000 euros.

La commission comprend la TVA, laquelle ne figure cependant pas sur la facture.

Calcul en cas d'imposition régulière:

Prix d'adjudication jusqu'à 800 000 € : 27 % de commission majorée de la TVA légale

Prix d'adjudication supérieur à 800 000 € : montants partiels jusqu'à 800 000 € 27 % de commission, montants partiels supérieurs à 800 000 € : 21 % de commission, à chaque fois majorés de la TVA légale.

Prix d'adjudication supérieur à 4.000 000 € : montants partiels supérieurs à 4.000 000 € : 15 % de commission, à chaque fois majorés de la TVA légale.

Si vous souhaitez appliquer l'imposition régulière, merci de bien vouloir le communiquer par écrit avant la facturation.

Calcul en cas de droit de suite:

Pour les œuvres originales d’arts plastiques et de photographie d’artistes vivants ou d’artistes décédés il y a moins de 70 ans, soumises au droit de suite, une rémunération au titre du droit de suite à hauteur des pourcentages indiqués au § 26, al. 2 de la loi allemande sur les droits d’auteur (UrhG) est facturée en sus pour compenser la rémunération liée au droit de suite due par le commissaire-priseur conformément au § 26 UrhG. À ce jour, elle est calculée comme suit :

4 pour cent pour la part du produit de la vente à partir de 400,00 euros et jusqu’à 50 000 euros,

3 pour cent supplémentaires pour la part du produit de la vente entre 50 000,01 et 200 000 euros,

1 pour cent supplémentaire pour la part entre 200 000,01 et 350 000 euros,

0,5 pour cent supplémentaire pour la part entre 350 000,01 et 500 000 euros et

0,25 pour cent supplémentaire pour la part au-delà de 500 000 euros.

Le total de la rémunération au titre du droit de suite pour une revente s’élève au maximum à 12 500 euros.

Calcul en cas d'imposition différentielle:

- Prix d’adjudication jusqu’à 800 000 euros : frais de vente 32 %.

- Des frais de vente de 27% sont facturés sur la partie du prix d’adjudication dépassant 800 000 euros. Ils sont additionnés aux frais de vente dus pour la partie du prix d’adjudication allant jusqu’à 800 000 euros.

- Des frais de vente de 22% sont facturés sur la partie du prix d’adjudication dépassant 4 000 000 euros. Ils sont additionnés aux frais de vente dus pour la partie du prix d’adjudication allant jusqu’à 4 000 000 euros.

La commission comprend la TVA, laquelle ne figure cependant pas sur la facture.

Calcul en cas d'imposition régulière:

Prix d'adjudication jusqu'à 800 000 € : 27 % de commission majorée de la TVA légale

Prix d'adjudication supérieur à 800 000 € : montants partiels jusqu'à 800 000 € 27 % de commission, montants partiels supérieurs à 800 000 € : 21 % de commission, à chaque fois majorés de la TVA légale.

Prix d'adjudication supérieur à 4.000 000 € : montants partiels supérieurs à 4.000 000 € : 15 % de commission, à chaque fois majorés de la TVA légale.

Si vous souhaitez appliquer l'imposition régulière, merci de bien vouloir le communiquer par écrit avant la facturation.

Calcul en cas de droit de suite:

Pour les œuvres originales d’arts plastiques et de photographie d’artistes vivants ou d’artistes décédés il y a moins de 70 ans, soumises au droit de suite, une rémunération au titre du droit de suite à hauteur des pourcentages indiqués au § 26, al. 2 de la loi allemande sur les droits d’auteur (UrhG) est facturée en sus pour compenser la rémunération liée au droit de suite due par le commissaire-priseur conformément au § 26 UrhG. À ce jour, elle est calculée comme suit :

4 pour cent pour la part du produit de la vente à partir de 400,00 euros et jusqu’à 50 000 euros,

3 pour cent supplémentaires pour la part du produit de la vente entre 50 000,01 et 200 000 euros,

1 pour cent supplémentaire pour la part entre 200 000,01 et 350 000 euros,

0,5 pour cent supplémentaire pour la part entre 350 000,01 et 500 000 euros et

0,25 pour cent supplémentaire pour la part au-delà de 500 000 euros.

Le total de la rémunération au titre du droit de suite pour une revente s’élève au maximum à 12 500 euros.